Chapter 3 Exponential Smoothing

We will now get into our first modeling, which are exponential smoothing models. They have been around for quite some time, but can still be useful if interested in one-step ahead forecasting.

In R, we are able to do Simple (or Single) Exponential Smoothing Models, Holt Exponential Smoothing Models and Holt-Winters Exponential Smoothing Models. We will be using the Steel data set and the airline data set to illustrate these models. Each of these are shown below.

3.1 Simple Exponential Smoothing

For Simple Exponential Smoothing Models (SES), we have only one component, referred to as the level component. \[\hat{Y}_{t+1}= L_{t}\\ L_{t} = \alpha Y_{t} + (1-\alpha)L_{t-1}\]

This is basically a weighted average with the last observation and the last predicted value. Since this only has a level component, forecasts from SES models will be a horizontal line (hence why this method is called “one-step ahead” forecasting).

Before modeling, be sure to divide your data into a training, validation and test (or at least training and test). The below code illustrates the Simple (Single) Exponential Smoothing Model.

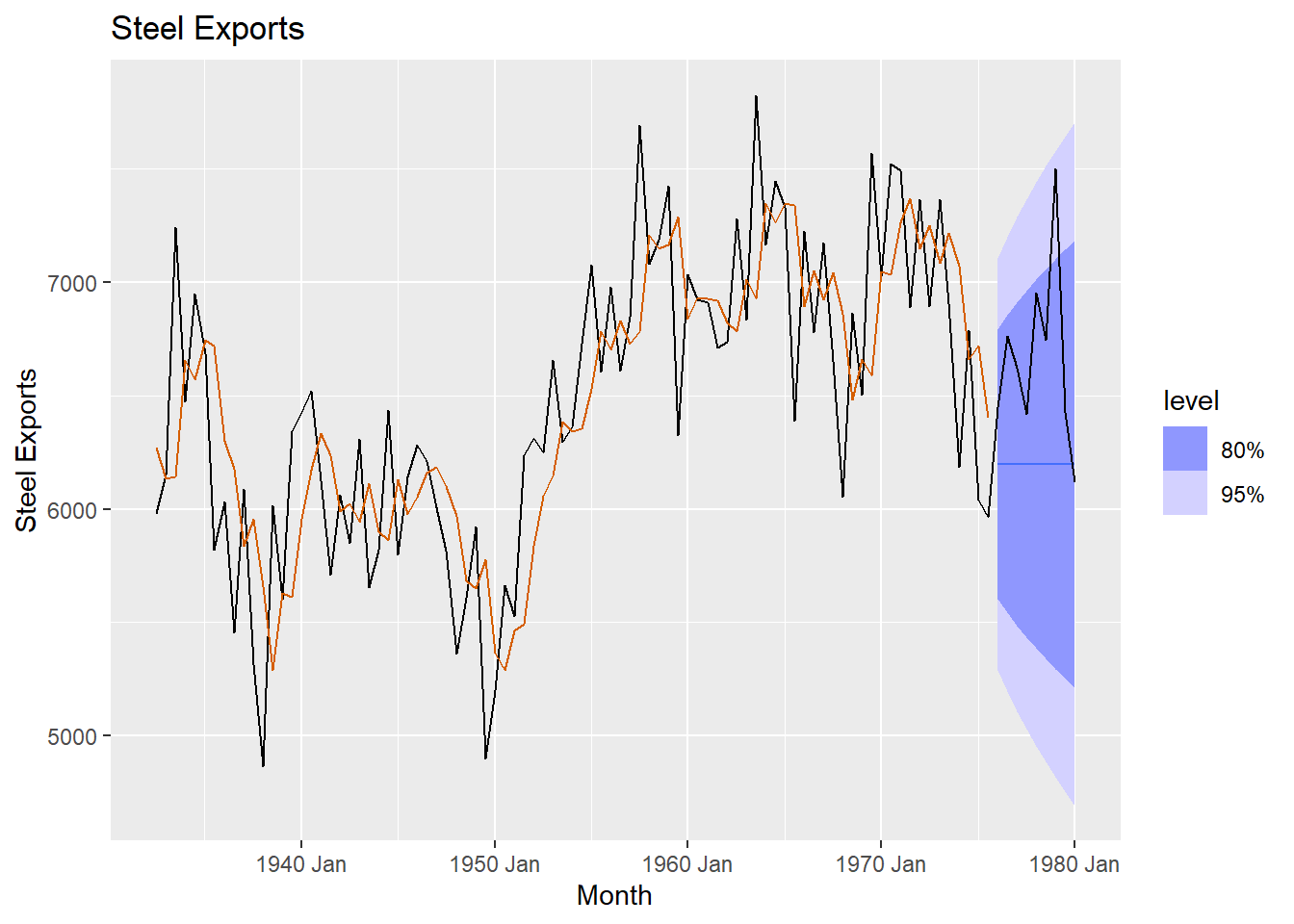

# Building a Single Exponential Smoothing (SES) Model - Steel Data #

Steel <- Steel |> mutate(date = seq(ymd('1932-07-01'),ymd('1980-01-01'),by='6 months'))

steel_ts<-Steel |> mutate(Month=yearmonth(date)) |> as_tsibble(index=Month)

steel_train <-steel_ts |> filter(year(date) <= 1975)

SES.Steel <- steel_train |>

model(ETS(steelshp ~ error("A") + trend("N") + season("N")))

Steel.for <- SES.Steel |>

fabletools::forecast(h = 9)

report(SES.Steel)## Series: steelshp

## Model: ETS(A,N,N)

## Smoothing parameters:

## alpha = 0.466543

##

## Initial states:

## l[0]

## 6269.498

##

## sigma^2: 214894.3

##

## AIC AICc BIC

## 1460.688 1460.977 1468.086# Plot the SES model on steel data

Steel.for |>

autoplot(steel_ts) +

geom_line(aes(y = .fitted), col="#D55E00",

data = augment(SES.Steel)) +

labs(y="Steel Exports", title="Steel Exports") +

guides(colour = "none")

# To get fitted values for training data set:

Steel_fitted <-fitted(SES.Steel)$.fitted

# To get fitted values for test data set:

Steel_test <- Steel.for$.mean

# Computes accuracy statistics for SES model on steel data (test data)

fabletools::accuracy(Steel.for, steel_ts)## # A tibble: 1 × 10

## .model .type ME RMSE MAE MPE MAPE MASE RMSSE ACF1

## <chr> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

## 1 "ETS(steelshp ~ error(\"A\") + trend(\"N\"… Test 468. 599. 486. 6.75 7.04 1.17 1.13 -0.05003.2 Holt ESM

The Holt model incorporates trend information. So, now there are two components: level and trend. For each component, there will be a smoothing coefficient (or weight). CAREFUL, when you look at parameter estimates, these are NOT the estimates for the mean nor the linear trend…you should be thinking of them as weights (between 0 and 1). The overall form for Holt’s method is:

\[\hat{Y}_{t+h}= L_{t}+hT_{t}\\ L_{t} = \alpha Y_{t} + (1-\alpha)(L_{t-1}+T_{t-1})\\ T_{t} = \beta (L_{t}-L_{t-1}) + (1-\beta) T_{t-1}\]

For the Holt’s method, when you forecast, you will see a trending line.

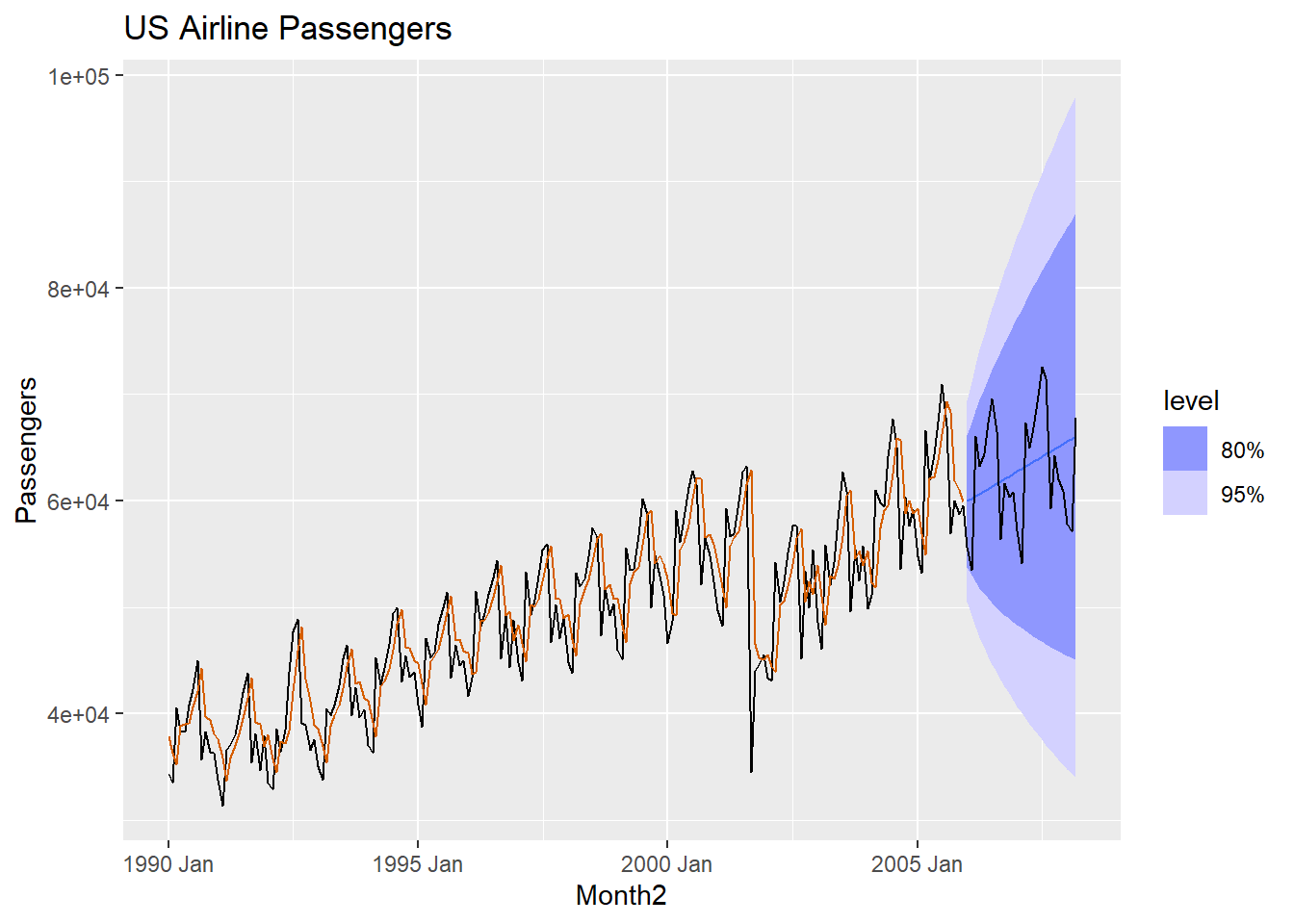

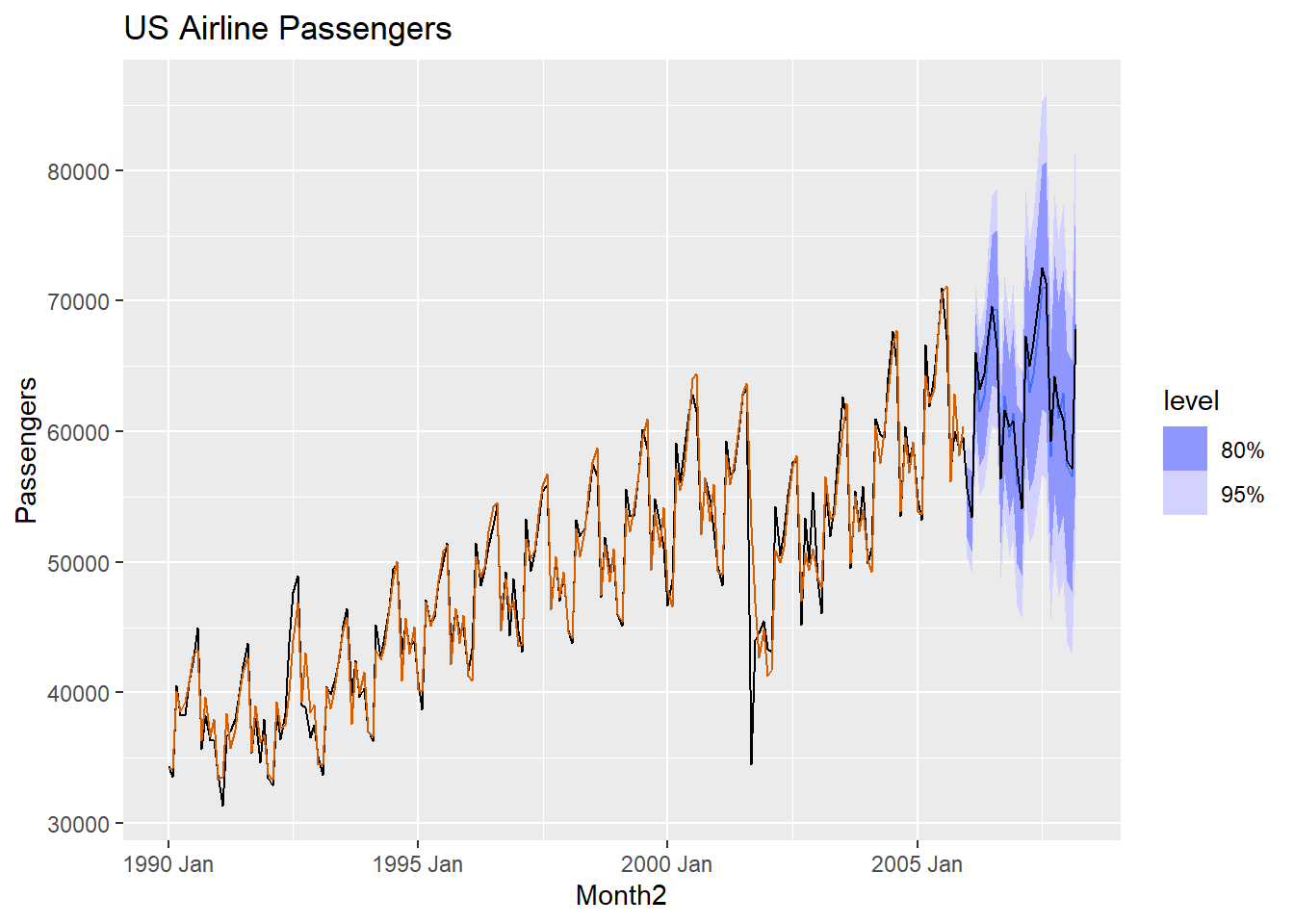

# Building a Linear Exponential Smoothing Model - US Airlines Data #

USAirlines_ts <- USAirlines |> mutate(date=myd(paste(Month, Year, "1"))) |> mutate(Month2=yearmonth(date)) |> as_tsibble(index=Month2)

air_train <-USAirlines_ts |> filter(year(date) <= 2005)

LES.air <- air_train |>

model(ETS(Passengers ~ error("A") + trend("A") + season("N")))

air.for <- LES.air |>

fabletools::forecast(h = 27)

report(LES.air)## Series: Passengers

## Model: ETS(A,A,N)

## Smoothing parameters:

## alpha = 0.5860139

## beta = 0.003740218

##

## Initial states:

## l[0] b[0]

## 37303.09 526.6595

##

## sigma^2: 23188824

##

## AIC AICc BIC

## 4271.560 4271.882 4287.847# Plot the data

air.for |>

autoplot(USAirlines_ts) +

geom_line(aes(y = .fitted), col="#D55E00",

data = augment(LES.air)) +

labs(y="Passengers", title="US Airline Passengers") +

guides(colour = "none")

We can also perform Holt’s method with a damped trend. You will see the formula for the damped trend is similar to the previous Holt formula with an addition of a dampening parameter.

\[\hat{Y}_{t+h}= L_{t}+\sum_{i}^{k}\phi^{i}T_{t}\\ L_{t} = \alpha Y_{t} + (1-\alpha)(L_{t-1}+\phi T_{t-1})\\ T_{t} = \beta (L_{t}-L_{t-1}) + (1-\beta) \phi T_{t-1}\]

We will illustrate the damped trend on the Airline data set.

LdES.air <- air_train |>

model(ETS(Passengers ~ error("A") + trend("Ad") + season("N")))

air.for <- LdES.air |>

fabletools::forecast(h = 27)

report(LdES.air)## Series: Passengers

## Model: ETS(A,Ad,N)

## Smoothing parameters:

## alpha = 0.5705768

## beta = 0.0001003564

## phi = 0.8085131

##

## Initial states:

## l[0] b[0]

## 36885.52 526.5046

##

## sigma^2: 23007825

##

## AIC AICc BIC

## 4271.031 4271.485 4290.576# Plot the data

air.for |>

autoplot(USAirlines_ts) +

geom_line(aes(y = .fitted), col="#D55E00",

data = augment(LdES.air)) +

labs(y="Passengers", title="US Airline Passengers") +

guides(colour = "none")

3.3 Holt-Winters

The Holt-Winters (HW) model has three components to it (level, trend and seasonality). Seasonality is an interesting component to model since we can have an additive seasonal component or a multiplicative seasonal component. Both models are shown below:

Additive HW \[\hat{Y}_{t+h}= L_{t}+hT_{t} + S_{t-p+h}\\ L_{t} = \alpha (Y_{t} - S_{t-p}) + (1-\alpha)(L_{t-1}+T_{t-1})\\ T_{t} = \beta (L_{t}-L_{t-1}) + (1-\beta) T_{t-1}\\ S_{t} = \gamma (Y_{t}-L_{t-1}-T_{t-1}) + (1-\gamma) S_{t-p}\]

Multiplicative HW \[\hat{Y}_{t+h}= (L_{t}+hT_{t}) S_{t-p+h}\\ L_{t} = \alpha \frac{Y_{t}} {S_{t-p}} + (1-\alpha)(L_{t-1}+T_{t-1})\\ T_{t} = \beta (L_{t}-L_{t-1}) + (1-\beta) T_{t-1}\\ S_{t} = \gamma \frac{Y_{t}}{L_{t-1}+T_{t-1}} + (1-\gamma) S_{t-p}\]

Where p is the frequency of the seasonality (i.e. how many “seasons” there are within one year).

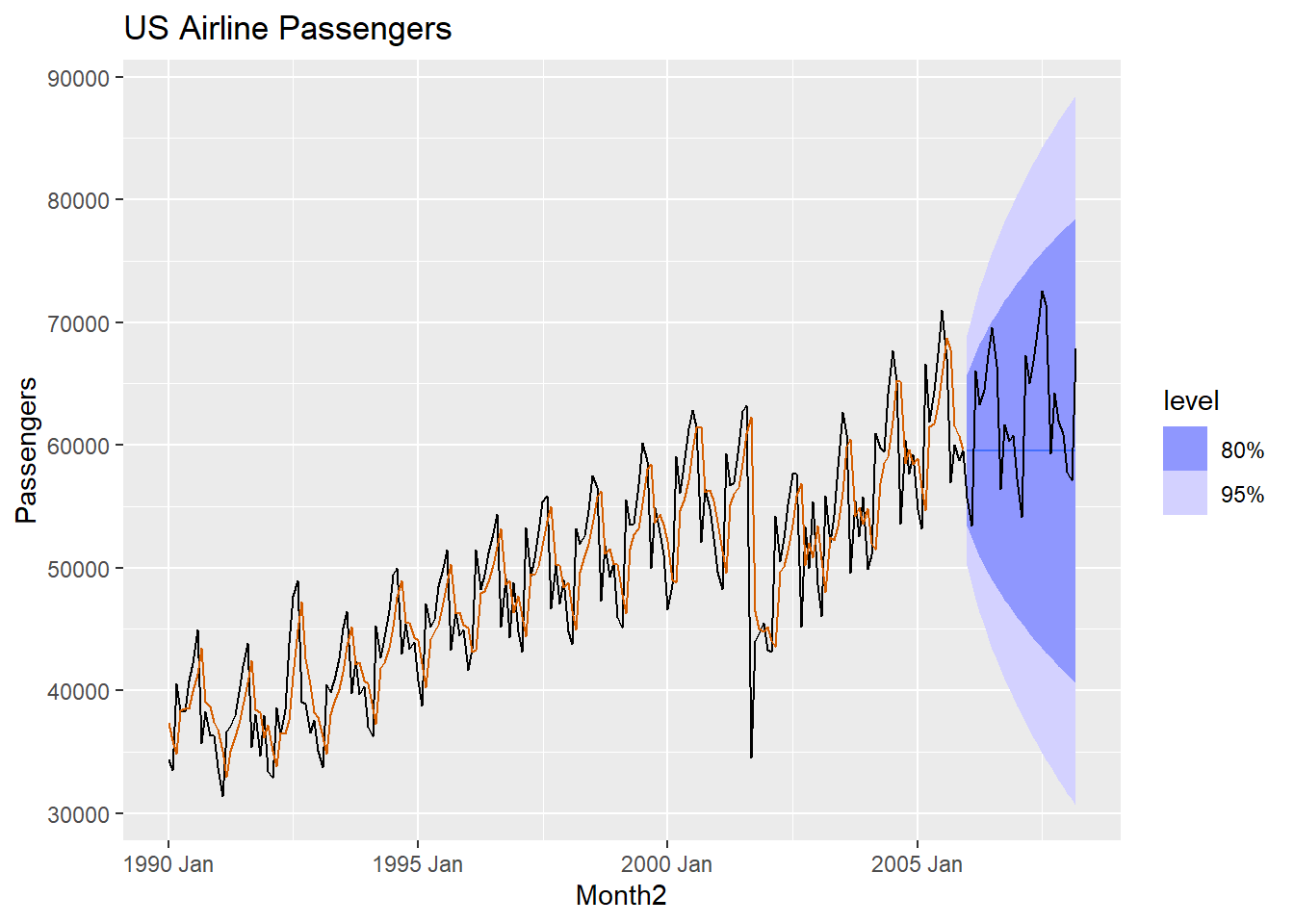

# Building a Holt-Winters ESM - US Airlines Data - Additive Seasonality

HWadd.air <- air_train |>

model(ETS(Passengers ~ error("A") + trend("A") + season("A")))

air.for <- HWadd.air |>

fabletools::forecast(h = 27)

report(HWadd.air)## Series: Passengers

## Model: ETS(A,A,A)

## Smoothing parameters:

## alpha = 0.5913618

## beta = 0.0001002723

## gamma = 0.0001000455

##

## Initial states:

## l[0] b[0] s[0] s[-1] s[-2] s[-3] s[-4] s[-5] s[-6] s[-7] s[-8]

## 38409 159.5944 -1520.744 -2728.928 -117.3477 -4305.732 6420.735 6299.852 4002.381 1210.882 122.2352

## s[-9] s[-10] s[-11]

## 2660.169 -6471.051 -5572.452

##

## sigma^2: 4099578

##

## AIC AICc BIC

## 3950.201 3953.718 4005.578# Plot the data

air.for |>

autoplot(USAirlines_ts) +

geom_line(aes(y = .fitted), col="#D55E00",

data = augment(HWadd.air)) +

labs(y="Passengers", title="US Airline Passengers") +

guides(colour = "none")

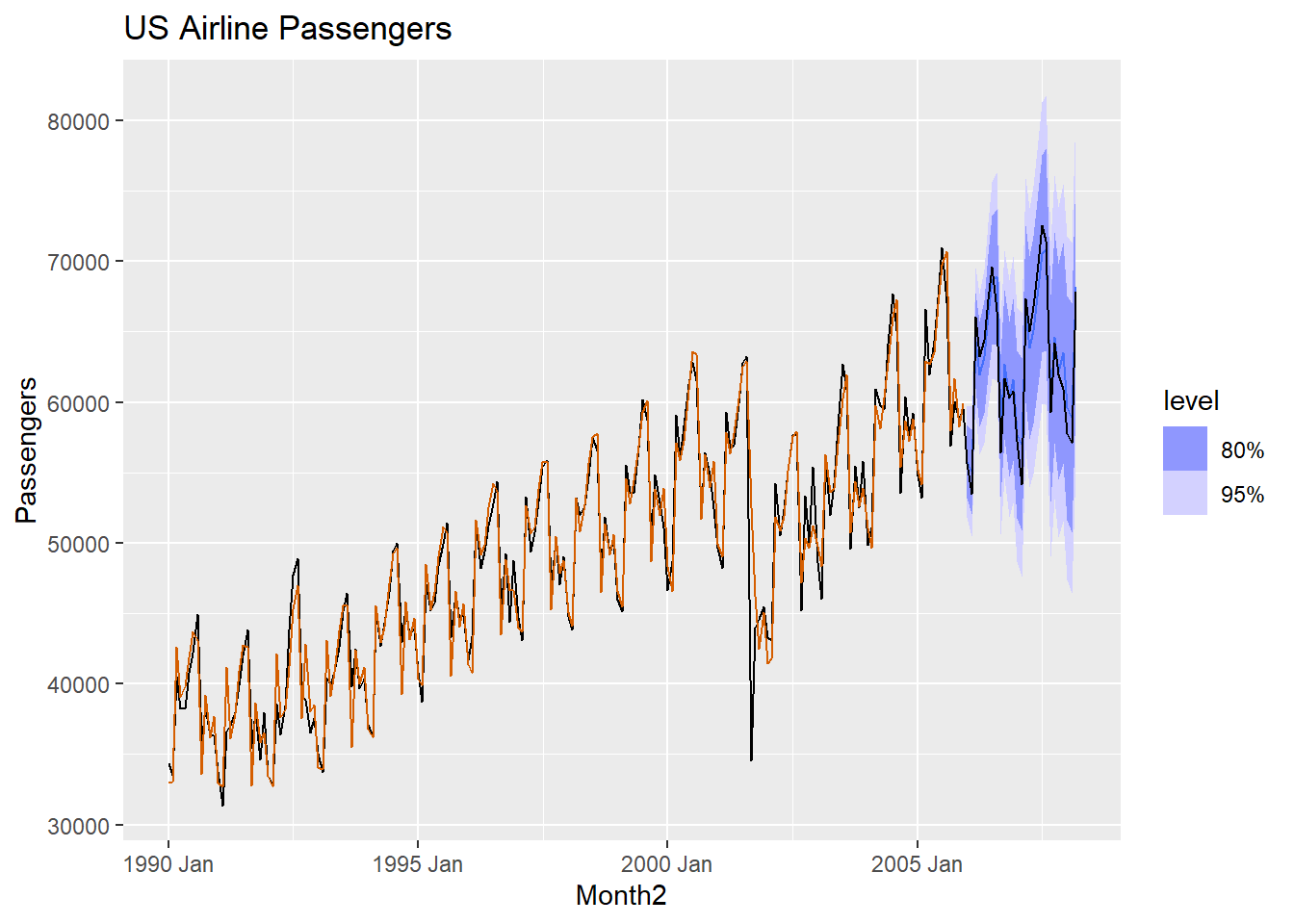

### Multiplicative model

HWmult.air <- air_train |>

model(ETS(Passengers ~ error("M") + trend("A") + season("M")))

air.for <- HWmult.air |>

fabletools::forecast(h = 27)

report(HWmult.air)## Series: Passengers

## Model: ETS(M,A,M)

## Smoothing parameters:

## alpha = 0.5132388

## beta = 0.006772624

## gamma = 0.0614166

##

## Initial states:

## l[0] b[0] s[0] s[-1] s[-2] s[-3] s[-4] s[-5] s[-6] s[-7]

## 38328.12 132.2916 0.9879613 0.9516784 1.015964 0.9248462 1.127338 1.111153 1.063682 1.012367

## s[-8] s[-9] s[-10] s[-11]

## 0.9931891 1.041972 0.8832477 0.8866022

##

## sigma^2: 0.0015

##

## AIC AICc BIC

## 3922.549 3926.066 3977.926# Plot the data

air.for |>

autoplot(USAirlines_ts) +

geom_line(aes(y = .fitted), col="#D55E00",

data = augment(HWmult.air)) +

labs(y="Passengers", title="US Airline Passengers") +

guides(colour = "none")

3.4 Comparing forecasts

This should be done on the validation data set (test data should ONLY be used ONCE…at the very end).

air_fit <- air_train |>

model(

SES = ETS(Passengers ~ error("A") + trend("N") + season("N")),

`Linear` = ETS(Passengers ~ error("A") + trend("A") + season("N")),

`Damped Linear` = ETS(Passengers ~ error("A") + trend("Ad") + season("N")),

HWAdd = ETS(Passengers ~ error("A") + trend("A") + season("A")),

HWMult = ETS(Passengers ~ error("M") + trend("A") + season("M"))

)

air_fc <- air_fit |>

fabletools::forecast(h = 27)

fabletools::accuracy(air_fc, USAirlines_ts)## # A tibble: 5 × 10

## .model .type ME RMSE MAE MPE MAPE MASE RMSSE ACF1

## <chr> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

## 1 Damped Linear Test 3351. 6251. 5238. 4.65 8.06 1.84 1.69 0.382

## 2 HWAdd Test -175. 1462. 1259. -0.421 2.02 0.443 0.395 0.448

## 3 HWMult Test 467. 1319. 1110. 0.705 1.75 0.391 0.356 0.219

## 4 Linear Test -67.3 5345. 4736. -0.789 7.62 1.67 1.44 0.436

## 5 SES Test 3346. 6248. 5236. 4.64 8.05 1.84 1.69 0.382Based upone this information, which model would you choose?

3.5 ETS

You can also allow the computer to search for the best model. The ETS (Error, Trend, Seasonality) algorithm will search for the best model and estimate the parameters. For the error term, we can have either an additive or multiplicative error structure. For the trend, we can have none, additive, or damped additive . For the seasonal component, we can have none, additive or multiplicative (lots of choices!). An example of how to run this is:

## Series: Passengers

## Model: ETS(M,Ad,M)

## Smoothing parameters:

## alpha = 0.6388447

## beta = 0.0001026043

## gamma = 0.0001060611

## phi = 0.979993

##

## Initial states:

## l[0] b[0] s[0] s[-1] s[-2] s[-3] s[-4] s[-5] s[-6] s[-7]

## 38326.08 97.13345 0.9672127 0.9438917 0.9983376 0.9209977 1.132478 1.132414 1.079442 1.022098

## s[-8] s[-9] s[-10] s[-11]

## 1.000804 1.051137 0.8657376 0.8854499

##

## sigma^2: 0.0014

##

## AIC AICc BIC

## 3910.149 3914.103 3968.784# Now compare this to the HW models:

air_fit <- air_train |>

model(

HWAdd = ETS(Passengers ~ error("A") + trend("A") + season("A")),

HWMult = ETS(Passengers ~ error("M") + trend("A") + season("M")),

AutoETS = ETS(Passengers ~ error("M") + trend("Ad") + season("M"))

)

air_fc <- air_fit |>

fabletools::forecast(h = 27)

fabletools::accuracy(air_fc, USAirlines_ts)## # A tibble: 3 × 10

## .model .type ME RMSE MAE MPE MAPE MASE RMSSE ACF1

## <chr> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

## 1 AutoETS Test 1734. 2343. 2020. 2.75 3.19 0.711 0.633 0.596

## 2 HWAdd Test -175. 1462. 1259. -0.421 2.02 0.443 0.395 0.448

## 3 HWMult Test 467. 1319. 1110. 0.705 1.75 0.391 0.356 0.219## Series: Passengers

## Model: ETS(M,N,M)

## Smoothing parameters:

## alpha = 0.7358545

## gamma = 0.001388497

##

## Initial states:

## l[0] s[0] s[-1] s[-2] s[-3] s[-4] s[-5] s[-6] s[-7] s[-8]

## 41491.07 0.9705455 0.9480705 0.9988812 0.9158342 1.119004 1.126052 1.073332 1.022722 1.003232

## s[-9] s[-10] s[-11]

## 1.057297 0.8713743 0.8936557

##

## sigma^2: 0.0015

##

## AIC AICc BIC

## 3912.504 3915.231 3961.3663.6 Python Code for Exponential Smoothing

The following Python codes will produce exponential smoothing models. The exponential smoothing models are using an older version in statsmodels (a new format is in statsforecast).

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

from matplotlib import pyplot

import seaborn as sns

from statsforecast.models import ETS

from statsforecast import StatsForecast

from statsforecast.utils import AirPassengers

from statsmodels.tsa.tsatools import detrend

from sklearn.metrics import mean_squared_error

from statsmodels.tsa.api import ExponentialSmoothing, SimpleExpSmoothing, Holt

from statsforecast.models import AutoETS

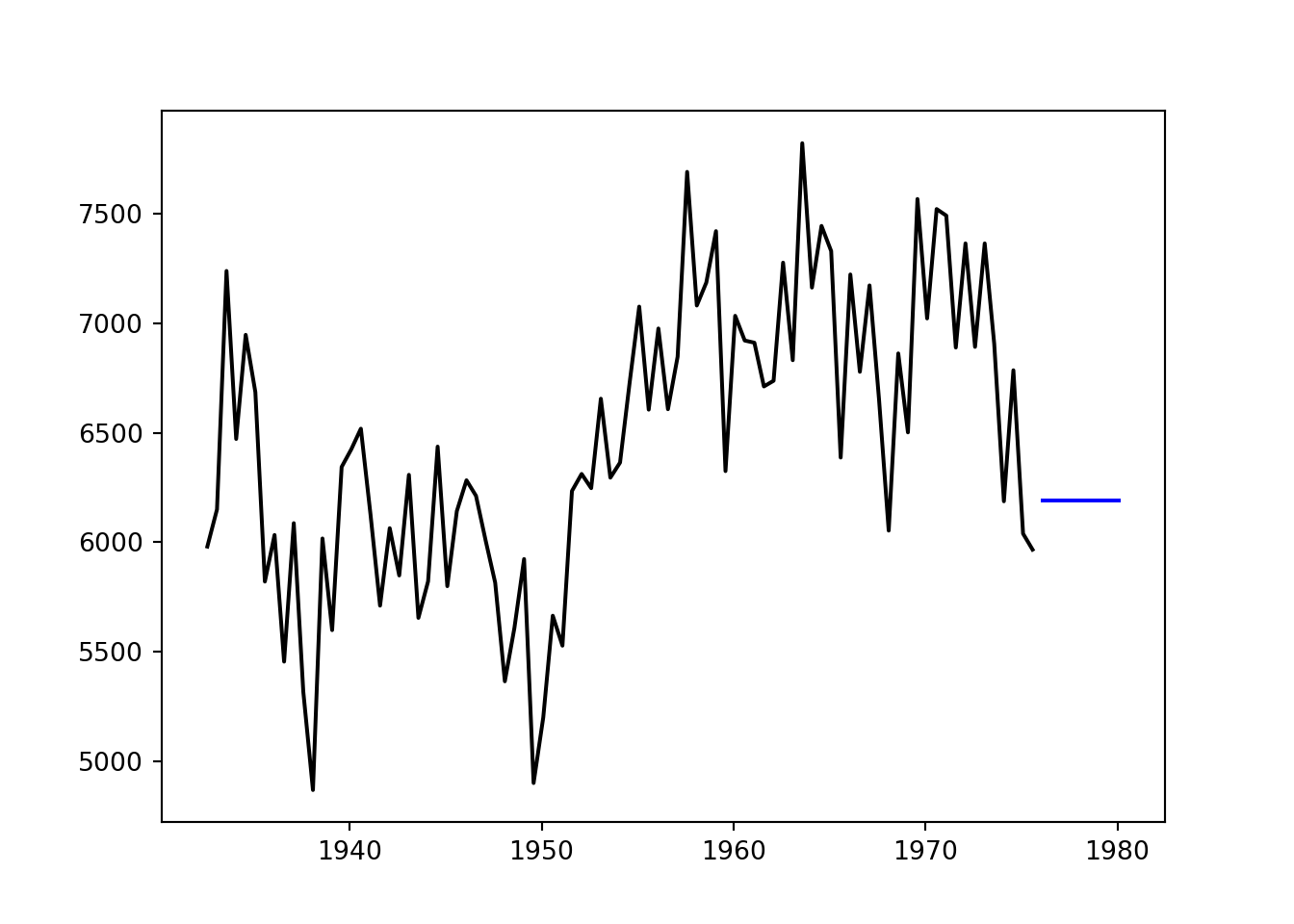

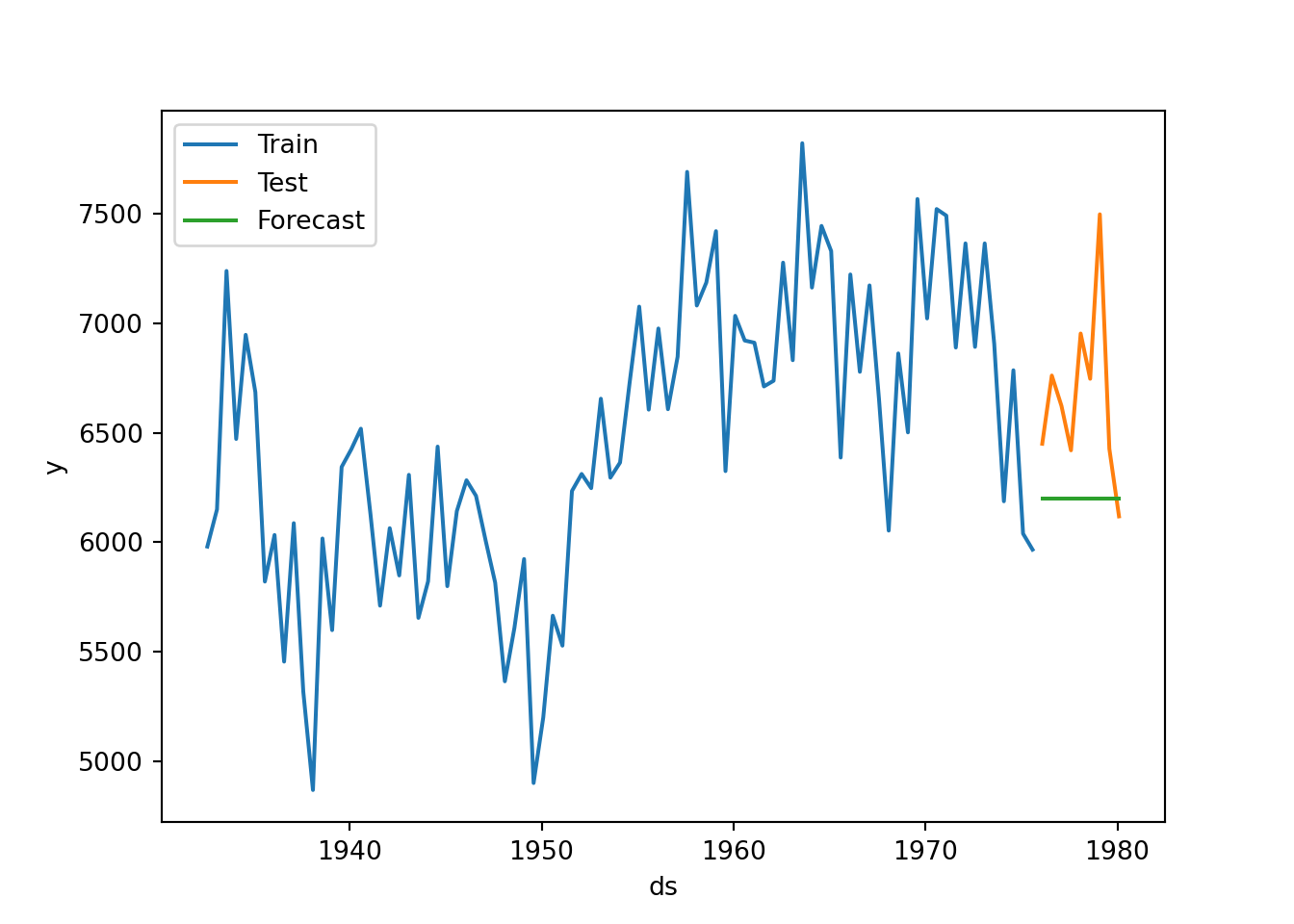

steel=pd.read_csv("Q:\\My Drive\\Fall 2017 - Time Series\\DataR\\steel.csv")

df = pd.date_range(start='1932-07-01', end='1980-07-01', freq='6ME')

steel.index=pd.to_datetime(df)

steel_train=steel.head(87)

steel_test = steel.tail(9)

fit = SimpleExpSmoothing(steel_train['steelshp']).fit()

fit.params['smoothing_level']## 0.4769767441860465## 1976-01-31 6188.807035

## 1976-07-31 6188.807035

## 1977-01-31 6188.807035

## 1977-07-31 6188.807035

## 1978-01-31 6188.807035

## 1978-07-31 6188.807035

## 1979-01-31 6188.807035

## 1979-07-31 6188.807035

## 1980-01-31 6188.807035

## Freq: 6ME, dtype: float64

##### Using Statsforecast

d = {'unique_id': 1, 'ds': steel.index, 'y': steel['steelshp']}

steel_sf = pd.DataFrame(data = d)

steel_train=steel_sf.head(87)

steel_test = steel_sf.tail(9)

steel_SES = StatsForecast(models = [AutoETS(model=["A","N","N"], alias="AutoETS", season_length=2)], freq = '6ME')

steel_model = steel_SES.fit(df = steel_train)

result = steel_SES.fitted_[0,0].model_['par']

result## array([4.66739272e-01, nan, nan, nan,

## 6.27096958e+03])## C:\PROGRA~3\ANACON~1\Lib\site-packages\statsforecast\core.py:492: FutureWarning: In a future version the predictions will have the id as a column. You can set the `NIXTLA_ID_AS_COL` environment variable to adopt the new behavior and to suppress this warning.

## warnings.warn(yhat=y_hat1.reset_index(drop=True)

forecast=pd.Series(pd.date_range("1976-01-31", freq="6ME", periods=9))

forecast=pd.DataFrame(forecast)

forecast.columns=["ds"]

forecast["hat"]=yhat['AutoETS']

forecast["unique_id"]="1"

sns.lineplot(steel_train,x="ds", y="y", label="Train")

sns.lineplot(steel_test, x="ds", y="y", label="Test")

sns.lineplot(forecast,x="ds", y="hat", label="Forecast",)

plt.show()

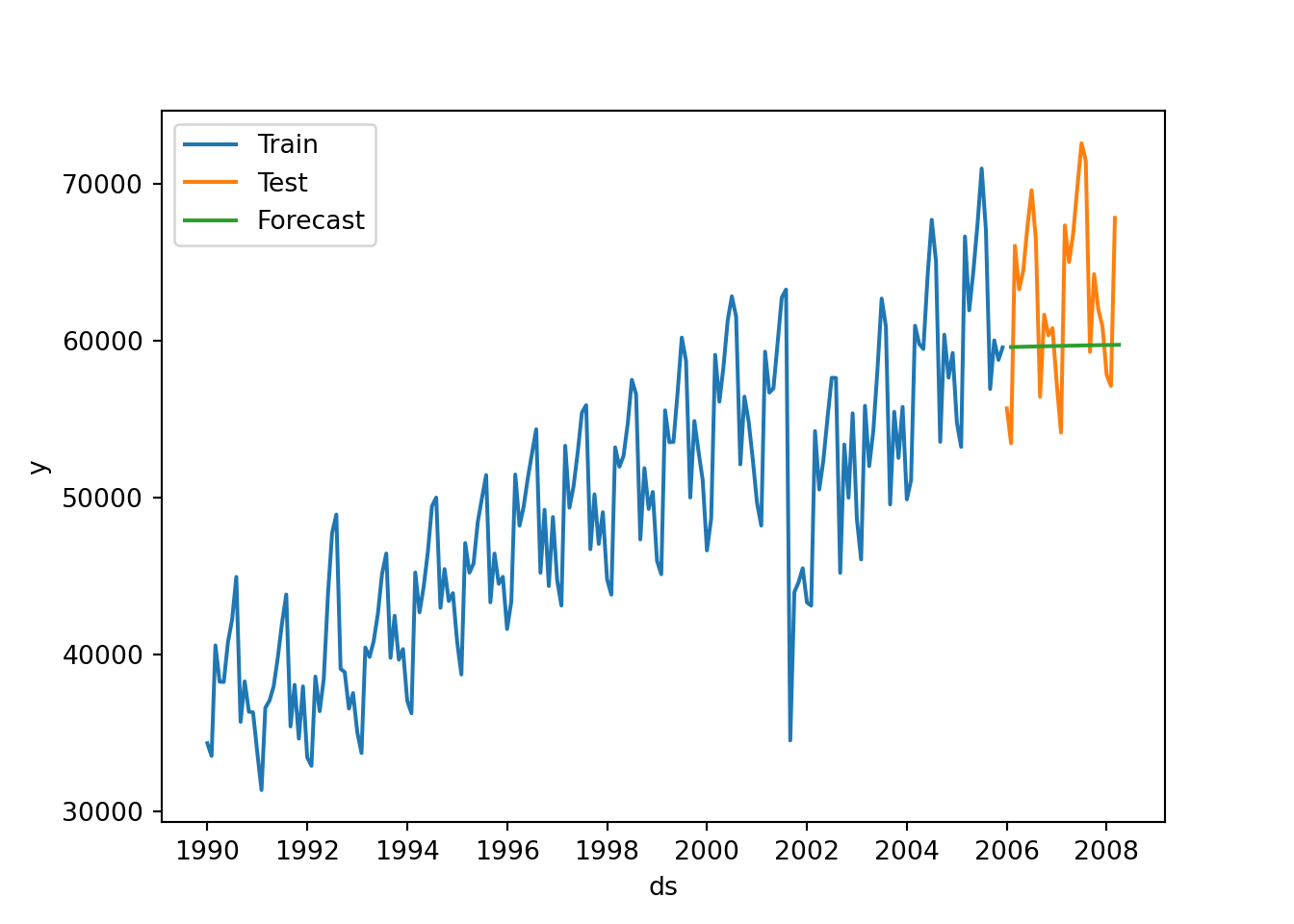

The Holt models in Python:

#### This code uses the new Statsforecast package

### Holt Model

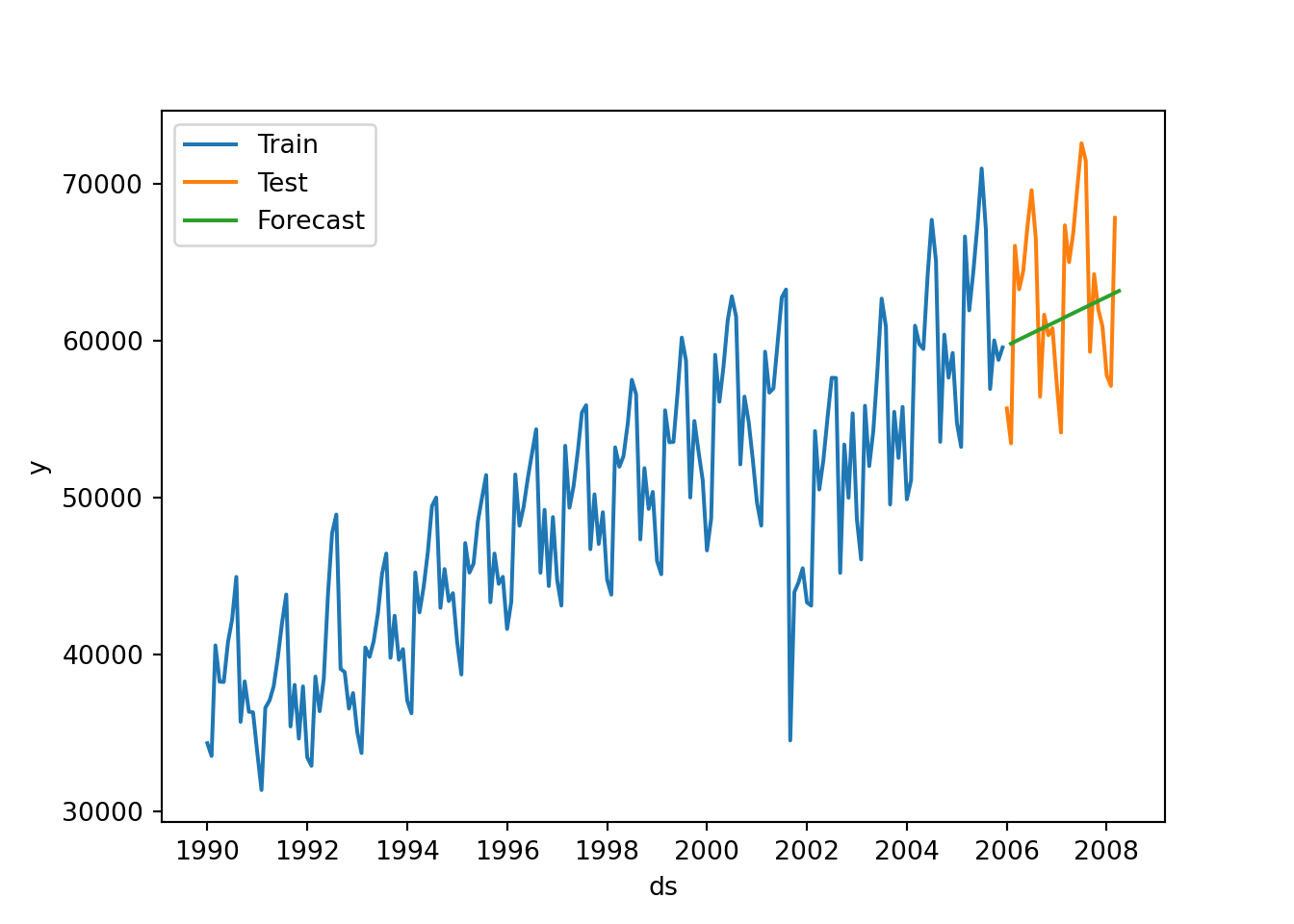

usair_p=pd.read_csv("Q:\\My Drive\\Fall 2017 - Time Series\\DataR\\usairlines.csv")

df=pd.date_range(start='1/1/1990', end='3/1/2008', freq='MS')

usair_p.index=pd.to_datetime(df)

d = {'unique_id': 1, 'ds': usair_p.index, 'y': usair_p['Passengers']}

usair_sf = pd.DataFrame(data = d)

### train has 192 observations

### test has 27 observations

air_train = usair_sf.head(192)

air_test = usair_sf.tail(27)

air_holt = StatsForecast(models = [AutoETS(model=["A","A","N"], alias="AutoETS", season_length=12)], freq = 'ME')

air_model = air_holt.fit(df = air_train)

result = air_holt.fitted_[0,0].model_['par']

result## array([5.69871723e-01, 1.00000000e-04, nan, nan,

## 3.48788866e+04, 1.29335525e+02])## C:\PROGRA~3\ANACON~1\Lib\site-packages\statsforecast\core.py:492: FutureWarning: In a future version the predictions will have the id as a column. You can set the `NIXTLA_ID_AS_COL` environment variable to adopt the new behavior and to suppress this warning.

## warnings.warn(yhat=y_hat1.reset_index(drop=True)

forecast=pd.Series(pd.date_range("2006-01-01", freq="ME", periods=27))

forecast=pd.DataFrame(forecast)

forecast.columns=["ds"]

forecast["hat"]=yhat['AutoETS']

forecast["unique_id"]="1"

sns.lineplot(air_train,x="ds", y="y", label="Train")

sns.lineplot(air_test, x="ds", y="y", label="Test")

sns.lineplot(forecast,x="ds", y="hat", label="Forecast",)

plt.show()

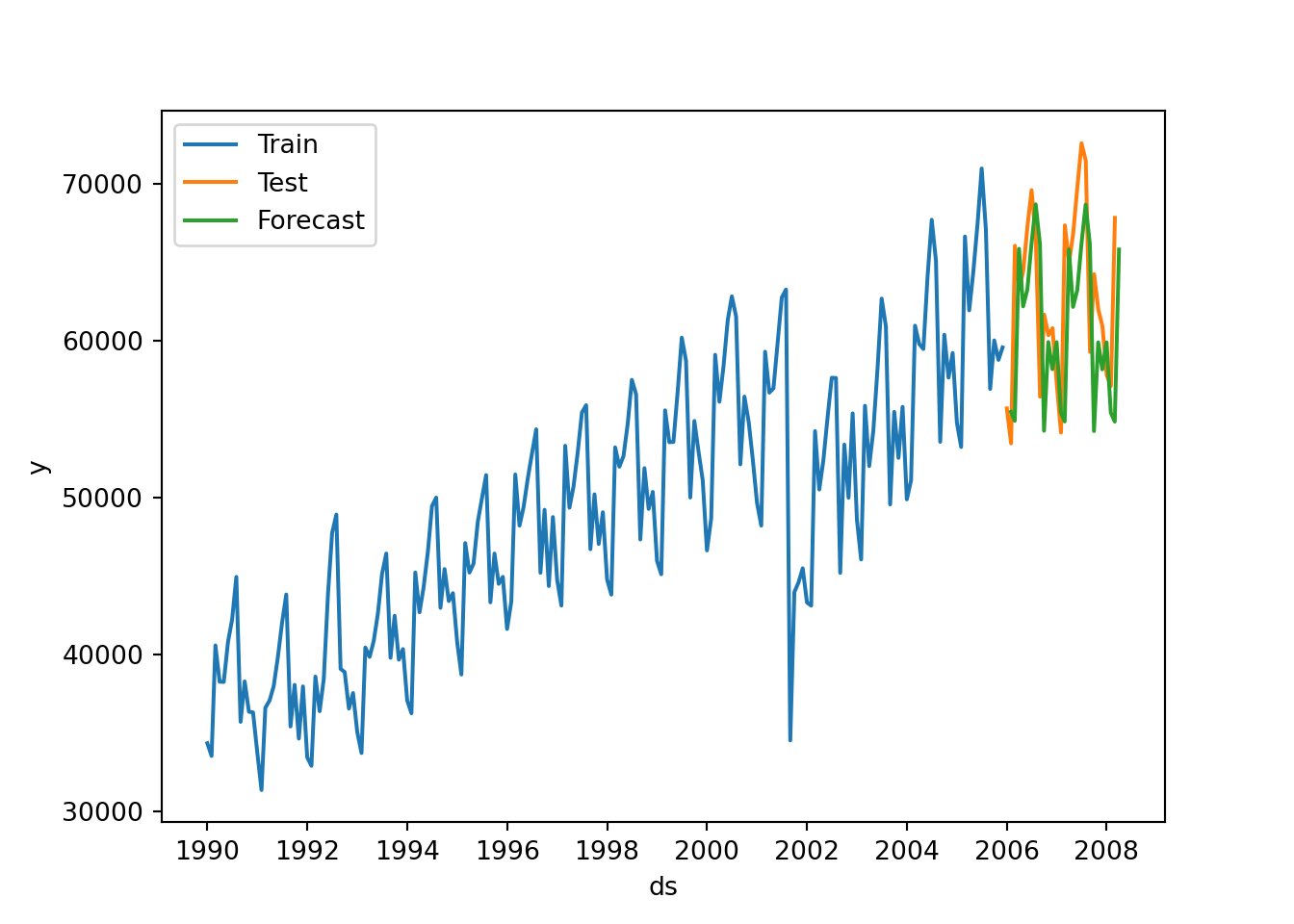

### Damped trend

air_holt = StatsForecast(models = [AutoETS(model=["A","A","N"], damped=True, alias="AutoETS", season_length=12)], freq = 'ME')

air_model = air_holt.fit(df = air_train)

result = air_holt.fitted_[0,0].model_['par']

result## array([5.71199778e-01, 1.00000000e-04, nan, 9.79993121e-01,

## 3.46022280e+04, 3.16699140e+02])## C:\PROGRA~3\ANACON~1\Lib\site-packages\statsforecast\core.py:492: FutureWarning: In a future version the predictions will have the id as a column. You can set the `NIXTLA_ID_AS_COL` environment variable to adopt the new behavior and to suppress this warning.

## warnings.warn(yhat=y_hat1.reset_index(drop=True)

forecast=pd.Series(pd.date_range("2006-01-01", freq="ME", periods=27))

forecast=pd.DataFrame(forecast)

forecast.columns=["ds"]

forecast["hat"]=yhat['AutoETS']

forecast["unique_id"]="1"

sns.lineplot(air_train,x="ds", y="y", label="Train")

sns.lineplot(air_test, x="ds", y="y", label="Test")

sns.lineplot(forecast,x="ds", y="hat", label="Forecast",)

plt.show()

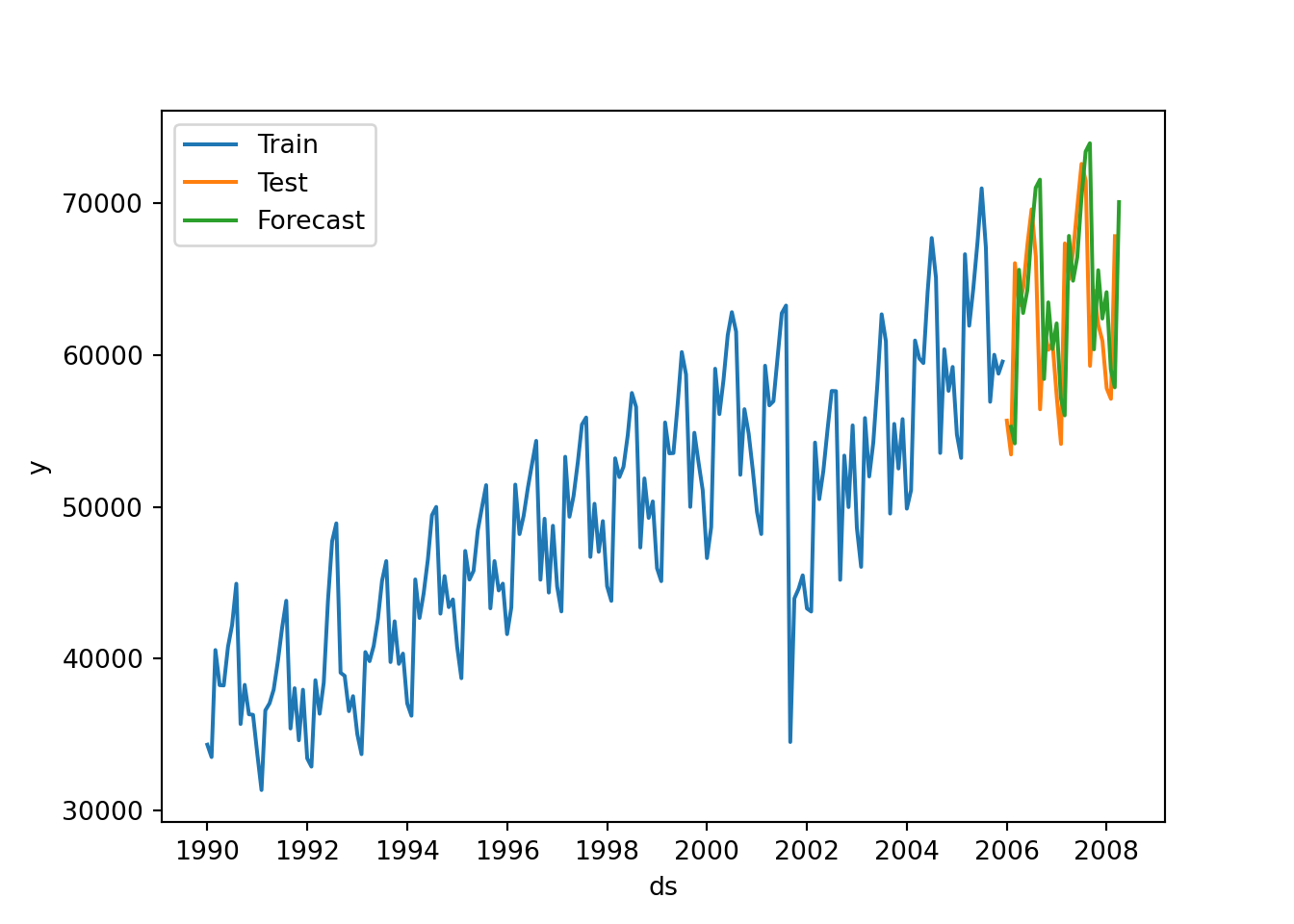

Seasonal models in Python:

### Using Statsforecast

### Additive Seasonality

air_holtw = StatsForecast(models = [AutoETS(model=["A","A","A"], alias="AutoETS", season_length=12)], freq = 'ME')

air_model = air_holtw.fit(df = air_train)

result = air_holtw.fitted_[0,0].model_['par']

result## array([ 4.81222943e-01, 1.59916114e-02, 2.42485779e-01, 8.90792825e-01,

## 3.77019540e+04, 5.67094839e+02, -9.99248746e+02, -2.53068050e+03,

## 1.17586756e+03, -2.77023876e+03, 5.79529172e+03, 4.08571477e+03,

## 2.44858026e+03, -1.89481694e+02, -5.21476747e+02, 1.96822431e+03,

## -4.80880072e+03, -3.65375146e+03])## C:\PROGRA~3\ANACON~1\Lib\site-packages\statsforecast\core.py:492: FutureWarning: In a future version the predictions will have the id as a column. You can set the `NIXTLA_ID_AS_COL` environment variable to adopt the new behavior and to suppress this warning.

## warnings.warn(yhat=y_hat1.reset_index(drop=True)

forecast=pd.Series(pd.date_range("2006-01-01", freq="ME", periods=27))

forecast=pd.DataFrame(forecast)

forecast.columns=["ds"]

forecast["hat"]=yhat['AutoETS']

forecast["unique_id"]="1"

sns.lineplot(air_train,x="ds", y="y", label="Train")

sns.lineplot(air_test, x="ds", y="y", label="Test")

sns.lineplot(forecast,x="ds", y="hat", label="Forecast",)

plt.show()

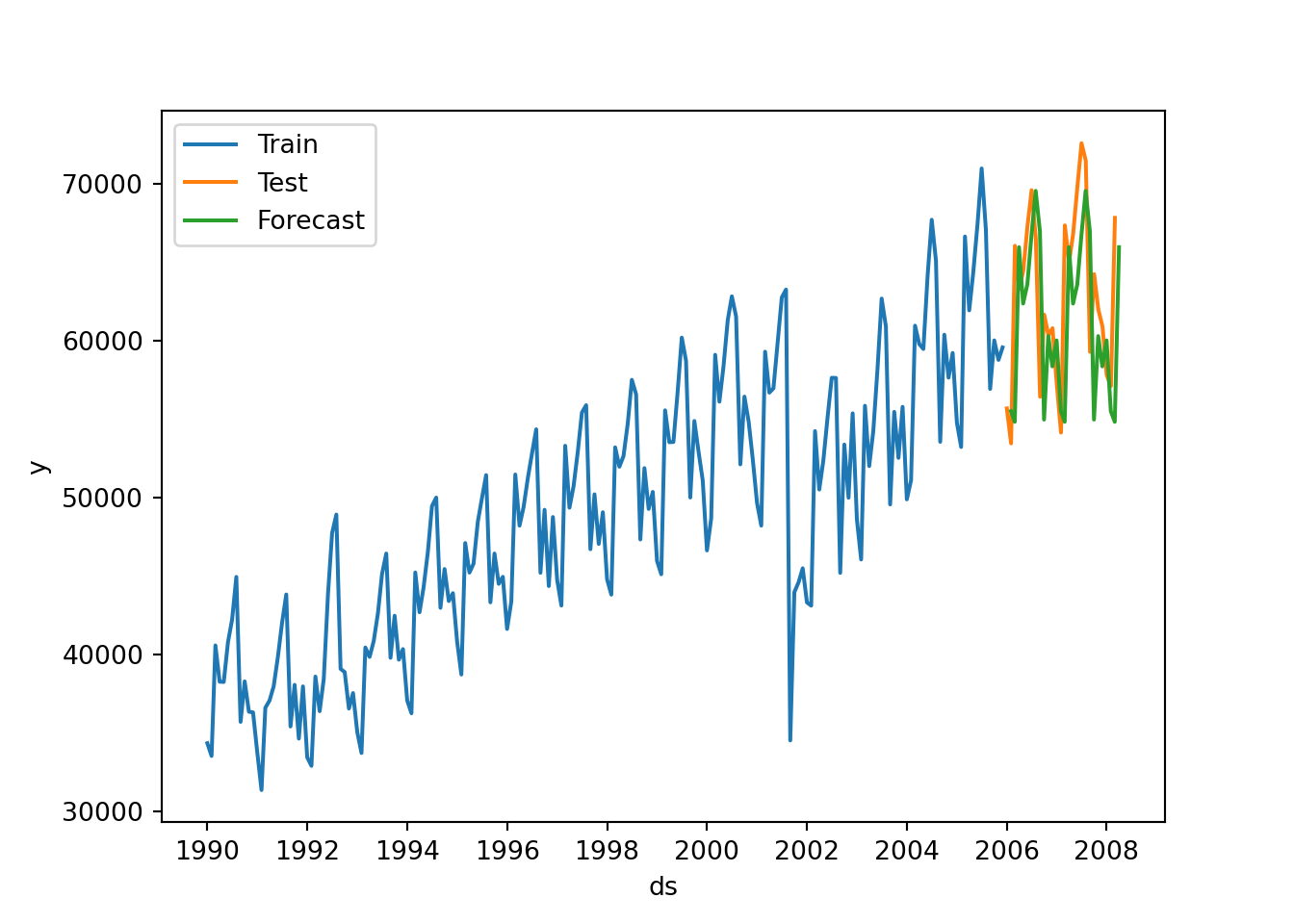

### Multiplicative Seasonality

air_holtw = StatsForecast(models = [AutoETS(model=["M","A","M"], alias="AutoETS", season_length=12)], freq = 'ME')

air_model = air_holtw.fit(df = air_train)

result = air_holtw.fitted_[0,0].model_['par']

result## array([9.45573068e-02, 2.64219583e-03, 2.54391669e-02, nan,

## 3.72394856e+04, 1.57545432e+02, 9.69302717e-01, 9.46292042e-01,

## 9.96735467e-01, 9.23896361e-01, 1.13023141e+00, 1.12016781e+00,

## 1.07916358e+00, 1.02341081e+00, 1.00200872e+00, 1.04798340e+00,

## 8.69839578e-01, 8.90968112e-01])## C:\PROGRA~3\ANACON~1\Lib\site-packages\statsforecast\core.py:492: FutureWarning: In a future version the predictions will have the id as a column. You can set the `NIXTLA_ID_AS_COL` environment variable to adopt the new behavior and to suppress this warning.

## warnings.warn(yhat=y_hat1.reset_index(drop=True)

forecast=pd.Series(pd.date_range("2006-01-01", freq="ME", periods=27))

forecast=pd.DataFrame(forecast)

forecast.columns=["ds"]

forecast["hat"]=yhat['AutoETS']

forecast["unique_id"]="1"

sns.lineplot(air_train,x="ds", y="y", label="Train")

sns.lineplot(air_test, x="ds", y="y", label="Test")

sns.lineplot(forecast,x="ds", y="hat", label="Forecast",)

plt.show()

### AutoETS

air_holtw = StatsForecast(models = [AutoETS(model=["Z","Z","Z"], alias="AutoETS", season_length=12)], freq = 'ME')

air_model = air_holtw.fit(df = air_train)

result = air_holtw.fitted_[0,0].model_['par']

result## array([ 3.53928248e-01, nan, 2.91330703e-01, nan,

## 3.88348407e+04, -8.30637153e+02, -2.79366612e+03, 3.48960549e+02,

## -1.64504368e+03, 6.41938336e+03, 5.16183884e+03, 2.80318982e+03,

## 1.24549104e+02, -1.04962061e+03, 9.50906067e+02, -5.57370399e+03,

## -3.91615619e+03])## C:\PROGRA~3\ANACON~1\Lib\site-packages\statsforecast\core.py:492: FutureWarning: In a future version the predictions will have the id as a column. You can set the `NIXTLA_ID_AS_COL` environment variable to adopt the new behavior and to suppress this warning.

## warnings.warn(yhat=y_hat1.reset_index(drop=True)

forecast=pd.Series(pd.date_range("2006-01-01", freq="ME", periods=27))

forecast=pd.DataFrame(forecast)

forecast.columns=["ds"]

forecast["hat"]=yhat['AutoETS']

forecast["unique_id"]="1"

sns.lineplot(air_train,x="ds", y="y", label="Train")

sns.lineplot(air_test, x="ds", y="y", label="Test")

sns.lineplot(forecast,x="ds", y="hat", label="Forecast",)

plt.show()

### Comparing models:

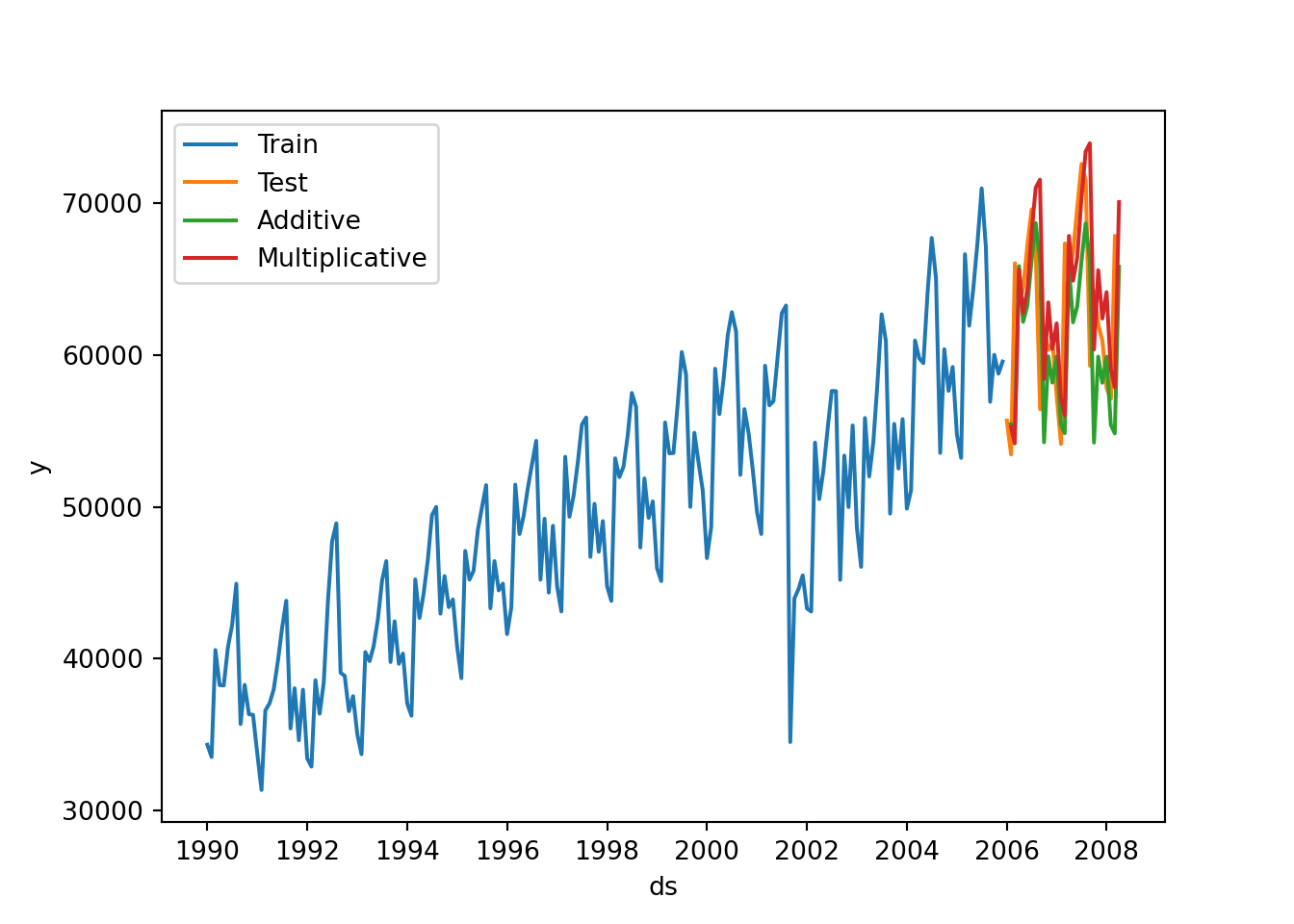

air_holtw = StatsForecast(models = [AutoETS(model=["A","A","A"], alias = "Additive", season_length=12),

AutoETS(model=["M","A","M"], alias = "Multiplicative", season_length=12)], freq = 'ME')

air_model = air_holtw.fit(df = air_train)

y_hat1=air_model.predict(h=27)## C:\PROGRA~3\ANACON~1\Lib\site-packages\statsforecast\core.py:492: FutureWarning: In a future version the predictions will have the id as a column. You can set the `NIXTLA_ID_AS_COL` environment variable to adopt the new behavior and to suppress this warning.

## warnings.warn(## ds Additive Multiplicative

## unique_id

## 1 2005-12-31 55463.046875 55276.296875

## 1 2006-01-31 54885.386719 54177.058594

## 1 2006-02-28 65846.859375 65606.875000

## 1 2006-03-31 62177.195312 62759.925781

## 1 2006-04-30 63248.167969 64265.078125

## 1 2006-05-31 66142.429688 67983.453125

## 1 2006-06-30 68683.671875 71003.070312

## 1 2006-07-31 66152.406250 71539.562500

## 1 2006-08-31 54251.707031 58415.742188

## 1 2006-09-30 59907.390625 63461.949219

## 1 2006-10-31 58180.179688 60389.761719

## 1 2006-11-30 59900.917969 62076.480469

## 1 2006-12-31 55417.457031 57164.699219

## 1 2007-01-31 54844.781250 56022.656250

## 1 2007-02-28 65810.687500 67835.507812

## 1 2007-03-31 62144.972656 64885.832031

## 1 2007-04-30 63219.460938 66435.843750

## 1 2007-05-31 66116.859375 70273.367188

## 1 2007-06-30 68660.890625 73388.007812

## 1 2007-07-31 66132.117188 73935.812500

## 1 2007-08-31 54233.632812 60366.957031

## 1 2007-09-30 59891.289062 65575.835938

## 1 2007-10-31 58165.839844 62395.746094

## 1 2007-11-30 59888.144531 64132.800781

## 1 2007-12-31 55406.078125 59053.101562

## 1 2008-01-31 54834.640625 57868.250000

## 1 2008-02-29 65801.656250 70064.148438## C:\PROGRA~3\ANACON~1\Lib\site-packages\statsforecast\core.py:492: FutureWarning: In a future version the predictions will have the id as a column. You can set the `NIXTLA_ID_AS_COL` environment variable to adopt the new behavior and to suppress this warning.

## warnings.warn(yhat=y_hat1.reset_index(drop=True)

forecast=pd.Series(pd.date_range("2006-01-01", freq="ME", periods=27))

forecast=pd.DataFrame(forecast)

forecast.columns=["ds"]

forecast["hat1"]=yhat['Additive']

forecast["hat2"]=yhat['Multiplicative']

forecast["unique_id"]="1"

sns.lineplot(air_train,x="ds", y="y", label="Train")

sns.lineplot(air_test, x="ds", y="y", label="Test")

sns.lineplot(forecast,x="ds", y="hat1", label="Additive")

sns.lineplot(forecast,x="ds", y="hat2", label="Multiplicative")

plt.show()

3.7 SAS Code for Exponential Smoothing Models

The following code is for Exponential Smoothing models in SAS.

Create library for data sets

libname Time ‘Q:Drive - Time Series’;

run;

SIMPLE EXPONENTIAL SMOOTHING MODEL

Create a simple exponential smoothing model

proc esm data=Time.Steel print=all plot=all lead=24;

forecast steelshp / model=simple;

run;

Create a simple exponential smoothing model with ID statement

proc esm data=Time.USAirlines print=all plot=all lead=24; id date interval=month; forecast Passengers / model=simple; run;

LINEAR TREND FOR EXPONENTIAL SMOOTHING

Double exponential smoothing

proc esm data=Time.Steel print=all plot=all lead=24; forecast steelshp / model=double; run;

linear exponential smoothing

proc esm data=Time.Steel print=all plot=all lead=24; forecast steelshp / model=linear; run;

damped trend exponential smoothing

proc esm data=Time.Steel print=all plot=all lead=24; forecast steelshp / model=damptrend; run;

linear exponential smoothign with interval = month

proc esm data=Time.USAirlines print=all plot=all lead=24; id date interval=month; forecast Passengers / model=linear; run;

SEASONAL EXPONENTIAL SMOOTHING MODEL

Additive seasonal exponential smoothing model

proc esm data=Time.USAirlines print=all plot=all seasonality=12 lead=24 outfor=test1; forecast Passengers / model=addseasonal; run;

mulitplicative seasonal exponential smoothing model

proc esm data=Time.USAirlines print=all plot=all seasonality=12 lead=24; forecast Passengers / model=multseasonal; run;

Winters additive exponential smoothing model (includes trend)

proc esm data=Time.USAirlines print=all plot=all seasonality=12 lead=24; forecast Passengers / model=addwinters; run;

Winters multiplicative exponential smoothing model (includes trend) (Lead = 24)

proc esm data=Time.USAirlines print=all plot=all seasonality=12 lead=24; forecast Passengers / model=multwinters; run;

Winters multiplicative exponential smoothing model (includes trend) Lead = 12

proc esm data=Time.USAirlines print=all plot=all lead=12 back=12 seasonality=12; forecast Passengers / model=multwinters; run;

EXPLORATION of SEASONAL EXPONENTIAL SMOOTHING MODEL

Winters multiplicative exponential smoothing model (includes trend) Lead = 12, uses outfor statement to output forecasts

proc esm data=Time.USAirlines print=all plot=all

seasonality=12 lead=12 back=12 outfor=test;

forecast Passengers / model=multwinters;

run;

calculate |error|/|actual value|

data test2; set test; if TIMEID>207; abs_error=abs(error); abs_err_obs=abs_error/abs(actual); run;

mean of |error|/|actual value| for this forecast

proc means data=test2 mean; var abs_error abs_err_obs; run;